ATLO Breakout Report

Investor Analysis

Investor Summary: Atmus Filtration Technologies (ATLO)

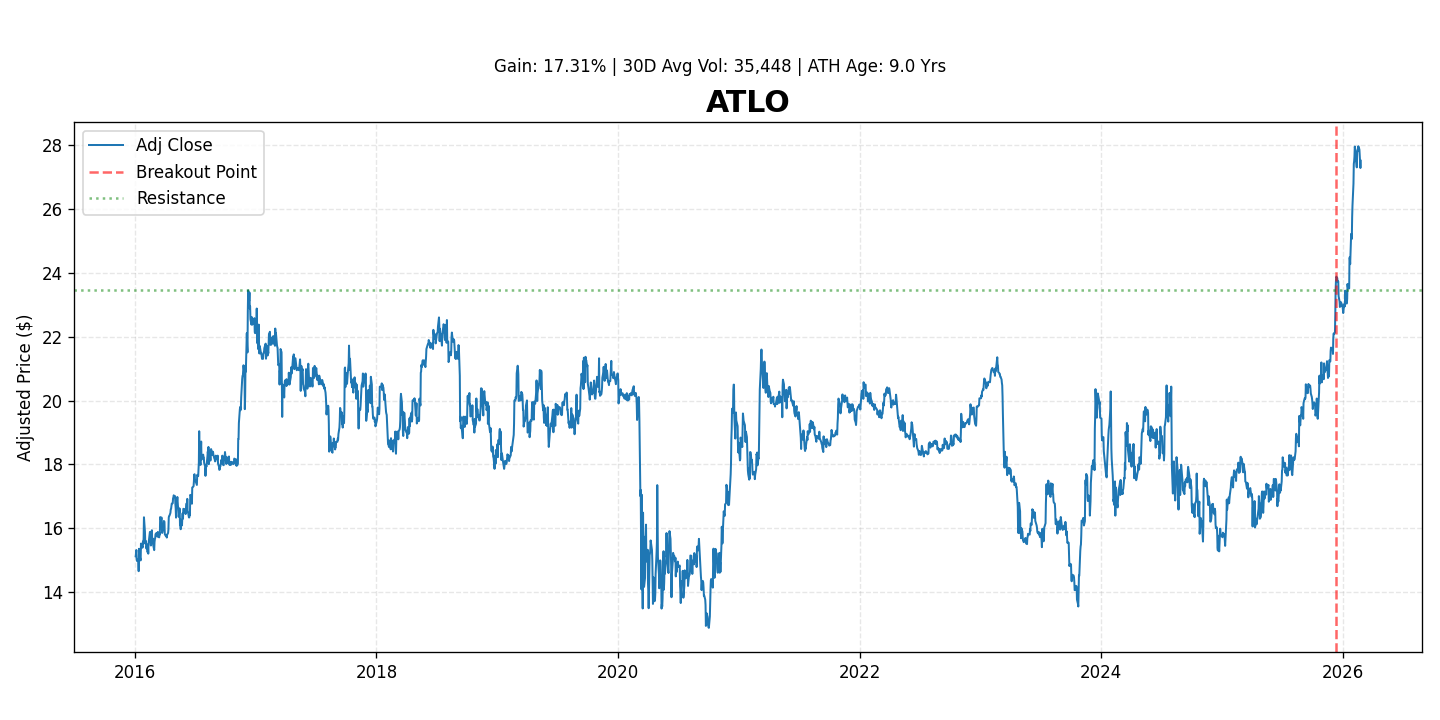

Atmus Filtration Technologies (ATLO) presents a compelling investment case, demonstrating strong strategic positioning and market momentum since its spin-off from Cummins in May 2023. The stock has exhibited robust performance, gaining an impressive 17.3% since its recent breakout, reflecting growing investor confidence in its pure-play filtration business model and resilient aftermarket revenue streams.

Business Overview

Atmus Filtration Technologies Inc. is a global leader in designing, manufacturing, and selling advanced filtration products. The company's comprehensive portfolio serves both on-highway and off-highway applications, including heavy-duty trucks, construction, mining, agriculture, and power generation equipment. Operating under its well-recognized Fleetguard brand, Atmus provides critical engine filtration (air, fuel, lube) and hydraulic filtration solutions, essential for equipment performance, reliability, and compliance with environmental regulations. Approximately 70% of the company's revenue is derived from the stable and recurring aftermarket segment.

Key Competitive Moats

- Market Leadership & Brand Strength: Atmus boasts a global presence and leverages the highly trusted Fleetguard brand, fostering deep relationships with major Original Equipment Manufacturers (OEMs) and a loyal aftermarket customer base.

- Technological Expertise: Extensive investment in Research & Development drives continuous innovation in filtration media and system design, enabling the company to meet increasingly stringent global emissions standards and enhance equipment longevity.

- High Switching Costs: As filtration is a mission-critical and highly engineered component, customers face significant risks and costs associated with switching from established, reliable suppliers, ensuring stable demand and customer retention.

- Extensive Global Footprint: A vast manufacturing, distribution, and service network facilitates efficient delivery and comprehensive support across diverse international geographies.

- Resilient Aftermarket Revenue: A substantial portion of Atmus's revenue is generated from high-margin replacement filters, providing stable, recurring cash flows that are less susceptible to fluctuations in new equipment sales cycles.

Revenue and Earnings Growth Outlook (Analyst Consensus)

Analyst consensus points to continued steady growth in both revenue and earnings for 2025 and 2026, driven by stable aftermarket demand, ongoing operational efficiencies, and strategic market penetration.

- Q1 2025 (ending March 31, 2025): Estimated Revenue: ~$400M - $410M; Estimated EPS: ~$0.45 - $0.50

- Q2 2025 (ending June 30, 2025): Estimated Revenue: ~$415M - $425M; Estimated EPS: ~$0.52 - $0.57

- Q3 2025 (ending September 30, 2025): Estimated Revenue: ~$420M - $430M; Estimated EPS: ~$0.55 - $0.60

- Q4 2025 (ending December 31, 2025): Estimated Revenue: ~$405M - $415M; Estimated EPS: ~$0.48 - $0.53

- Q1 2026 (ending March 31, 2026): Estimated Revenue: ~$410M - $420M; Estimated EPS: ~$0.48 - $0.53

Recent Catalysts

- Successful Spin-off from Cummins (May 2023): The separation allowed ATLO to operate as a focused, independent entity, unlocking potential for optimized capital allocation, strategic growth initiatives, and clearer market valuation.

- Strong Financial Performance: Consistent delivery of solid earnings reports, frequently exceeding analyst expectations, has bolstered investor confidence and underlined operational strength.

- Inclusion in S&P MidCap 400 Index (February 2024): This key development enhanced the company's market visibility, liquidity, and attracted broader institutional ownership.

- Favorable Market Re-evaluation: The market is increasingly recognizing Atmus's robust aftermarket business model, strong free cash flow generation, and attractive valuation as a pure-play industrial leader.

- Operational Efficiency Improvements: Post-spin initiatives focused on cost optimization, supply chain resilience, and manufacturing efficiency are contributing to margin expansion and improved profitability.

Main Risks

- Cyclicality of End Markets: Demand for both new equipment and subsequent aftermarket filters is inherently tied to the cyclical nature of the construction, mining, agriculture, and transportation sectors, which can be impacted by economic downturns.

- Raw Material Cost Volatility: Fluctuations in the prices of key raw materials (e.g., steel, specialized filtration media, resins) could exert pressure on the company's cost of goods sold and, consequently, its profitability.

- OEM Concentration: While Atmus is diversifying its customer base, a significant portion of its OEM revenue remains concentrated with a few large customers, including its former parent Cummins.

- Intense Competitive Pressures: The filtration market is competitive, with established global players and niche specialists potentially impacting market share and pricing power.

- Global Supply Chain Disruptions: Geopolitical events, trade tensions, or natural disasters could disrupt manufacturing, sourcing of components, and distribution networks, affecting production and delivery timelines.

Disclaimer: This summary is based on publicly available information and analyst consensus estimates, which are subject to change. It is not financial advice, and investors should conduct their own thorough due diligence. Forward-looking statements are inherently subject to various risks and uncertainties.

```