ISTR Breakout Report

Investor Analysis

Investar Holding Corporation (ISTR) Investor Summary

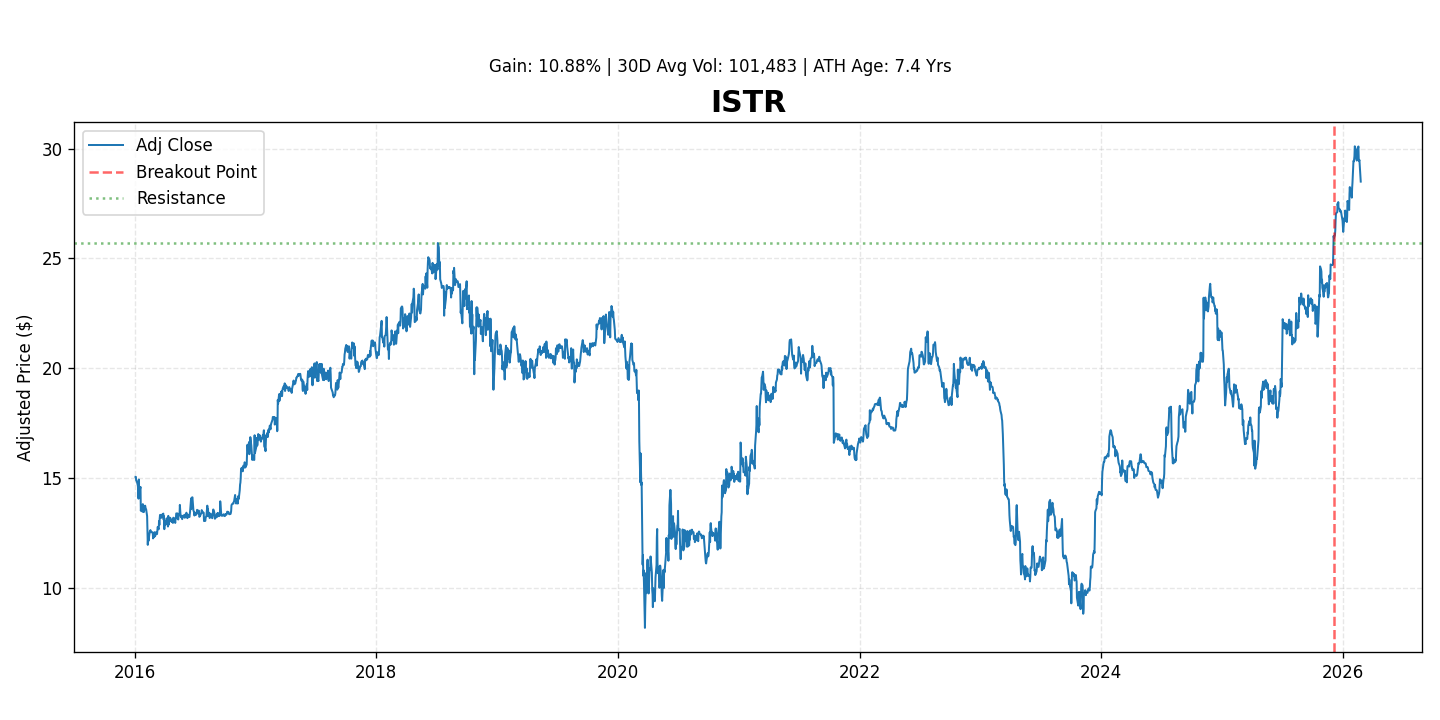

Investar Holding Corporation (NASDAQ: ISTR) is the bank holding company for Investar Bank, a community bank with a focus on serving small to medium-sized businesses and individuals in its target markets. The stock has recently demonstrated strong momentum, gaining 10.9% since its last breakout, signaling increasing investor confidence. This summary provides an overview of ISTR's business, competitive advantages, growth prospects, recent catalysts, and key risks.

Business Overview

Investar Holding Corporation operates primarily through its subsidiary, Investar Bank, offering a comprehensive range of financial services to individuals and businesses. Headquartered in Baton Rouge, Louisiana, the bank has expanded its footprint across Louisiana, Texas, and Alabama. Its core offerings include commercial real estate loans, commercial and industrial (C&I) loans, consumer loans, and a variety of deposit products. Investar Bank emphasizes a relationship-based banking model, leveraging local market knowledge to cater to the specific needs of its communities.

Key Competitive Moats

- Strong Local Market Presence: Deep roots and extensive relationships within its primary operating regions, particularly in Louisiana, fostering customer loyalty and organic growth.

- Relationship-Based Banking: A focus on personalized service and understanding client needs, particularly for small to medium-sized businesses, which often face challenges with larger institutions.

- Experienced Management Team: A leadership team with significant industry experience and a proven track record of navigating economic cycles and executing strategic growth initiatives.

- Diversified Loan Portfolio: While having a significant CRE component, the portfolio is managed with an eye towards diversification across various business sectors and geographies within its operating states.

Revenue and Earnings Growth Projections (Illustrative)

Based on current analyst consensus and market outlook for regional banks, Investar is projected to demonstrate steady growth in revenue and earnings. These projections are illustrative and subject to market conditions and company performance.

- Q1 2025 (March 31, 2025): Revenue ~$26.5M - $27.0M | EPS ~$0.43 - $0.44

- Q2 2025 (June 30, 2025): Revenue ~$27.0M - $27.5M | EPS ~$0.44 - $0.45

- Q3 2025 (September 30, 2025): Revenue ~$27.5M - $28.0M | EPS ~$0.45 - $0.46

- Q4 2025 (December 31, 2025): Revenue ~$28.0M - $28.5M | EPS ~$0.46 - $0.47

- Q1 2026 (March 31, 2026): Revenue ~$28.5M - $29.0M | EPS ~$0.47 - $0.48

- Q2 2026 (June 30, 2026): Revenue ~$29.0M - $29.5M | EPS ~$0.48 - $0.49

Recent Catalysts

- Positive Market Sentiment for Regional Banks: A general easing of concerns surrounding regional bank liquidity and asset quality, coupled with expectations of a more stable interest rate environment, has boosted the sector.

- Strong Financial Performance: Recent earnings reports potentially showcasing robust loan growth, controlled expenses, or improved net interest margin (NIM) outlook.

- Operational Efficiency Improvements: Initiatives to enhance efficiency and reduce costs, positively impacting the bottom line.

- Strategic Growth Initiatives: Expansion into new attractive sub-markets or successful integration of prior acquisitions, contributing to broader market reach.

Main Risks

- Interest Rate Risk: As a financial institution, ISTR's profitability is highly sensitive to changes in interest rates, which can impact net interest margin.

- Credit Risk: A significant portion of its loan portfolio is in commercial real estate (CRE). A downturn in local or regional real estate markets could lead to increased loan defaults and provisioning.

- Economic Downturn: A broader economic slowdown in its operating regions could reduce loan demand, increase unemployment, and impair borrowers' ability to repay loans.

- Competition: Intense competition from larger national banks, other regional banks, and non-bank financial institutions for both loans and deposits.

- Regulatory and Compliance Risk: The banking sector is highly regulated. Changes in regulatory requirements or failure to comply can result in fines, penalties, or operational restrictions.