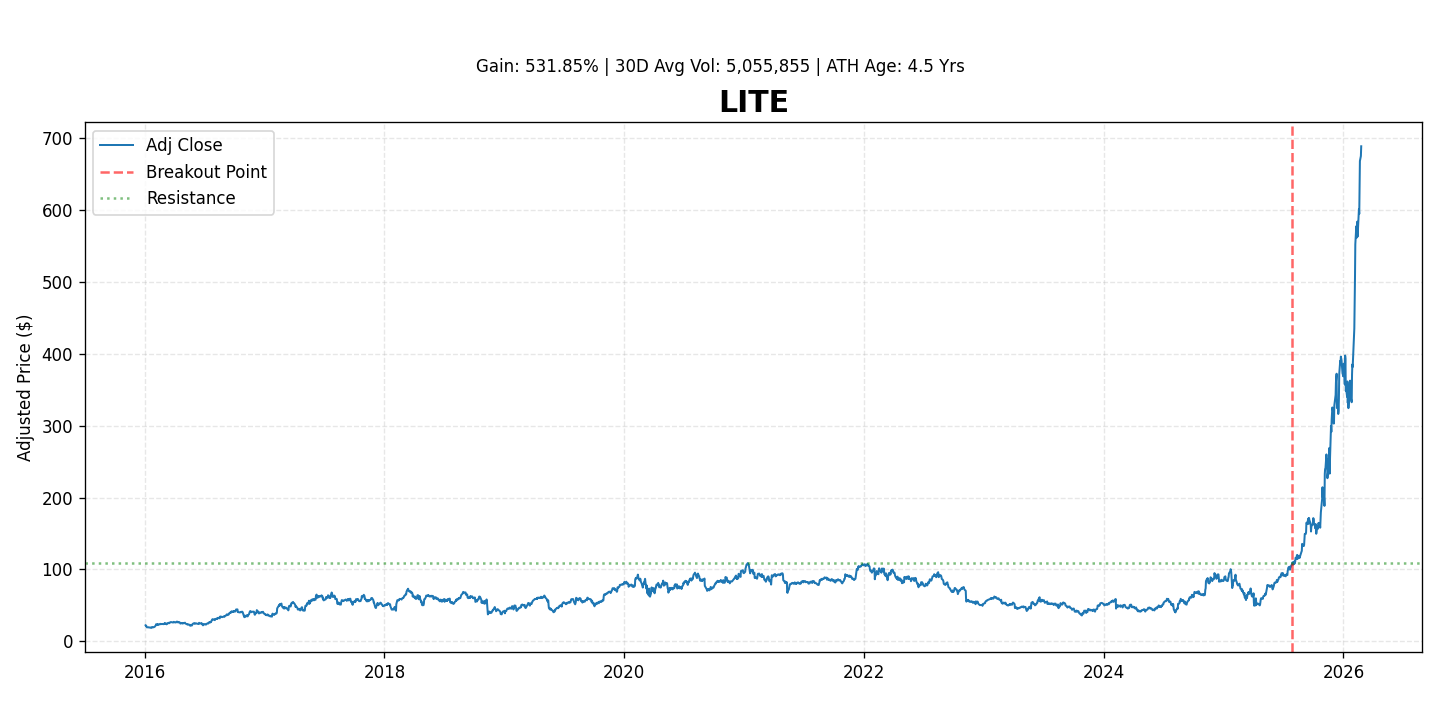

LITE Breakout Report

4.5 YrsAge

+531.8%Gain

5,055,85530D Vol

Investor Analysis

### Investor Summary: Lumentum Holdings Inc. (LITE)

Lumentum Holdings Inc. (LITE) is a leading designer and manufacturer of innovative optical and photonic products for use in optical networks and commercial lasers for manufacturing processes and various emerging applications. The company plays a critical role in global connectivity, advanced manufacturing, and next-generation technologies. While the stock has experienced significant appreciation, gaining 531.8% since its breakout, the focus for investors remains on its forward-looking growth trajectory, particularly driven by demand in AI infrastructure, telecom network upgrades, and industrial applications.

### Business Overview

Lumentum is structured around two primary segments: Optical Communications and Commercial Lasers. The **Optical Communications** segment provides a broad portfolio of components, modules, and subsystems for telecom and data communications networks, enabling high-speed data transmission crucial for cloud computing, 5G, and the burgeoning Artificial Intelligence (AI) ecosystem. Key products include tunable optical transceivers, reconfigurable optical add/drop multiplexers (ROADMs), and coherent modules. The **Commercial Lasers** segment offers a diverse range of lasers, including fiber lasers, diode lasers, and ultrafast lasers, used in precision manufacturing, biomedical applications, and scientific research. The company's innovative photonic technologies underpin much of the digital infrastructure and advanced industrial processes globally.

### Key Competitive Moats

* **Technology Leadership & Intellectual Property:** Lumentum possesses a robust portfolio of patents and deep expertise in optical and photonic innovation, allowing it to develop proprietary, high-performance products that are difficult for competitors to replicate.

* **Tier-1 Customer Relationships:** The company maintains strong, long-standing relationships with leading global network equipment manufacturers, data center operators, and industrial customers, often integrating its products deeply into their supply chains and product development cycles.

* **Manufacturing Scale & Vertical Integration:** Lumentum benefits from significant manufacturing scale and strategic vertical integration, which provides cost efficiencies, quality control, and supply chain resilience, differentiating it from smaller competitors.

* **Diversified Product Portfolio:** A broad offering across telecom, datacom, and industrial laser markets, coupled with exposure to emerging technologies like AI/ML, reduces reliance on any single market segment and provides multiple avenues for growth.

### Revenue and Earnings Growth Projections (2025/2026 Quarters)

Lumentum's growth is anticipated to be driven by a recovery in the telecom sector, continued robust demand from data centers (especially for AI applications), and stable growth in its industrial laser business. Analyst consensus projects a strong rebound and sustained growth for the company's fiscal years (FY, ending June 29). The following represent consensus analyst estimates and expected trends:

* **Calendar Q3 2024 (FY25 Q1):** Revenue estimated around $360M - $380M, with EPS around $0.35 - $0.45, reflecting initial signs of market stabilization and early AI-driven demand.

* **Calendar Q4 2024 (FY25 Q2):** Revenue projected to improve to $400M - $430M, with EPS of $0.60 - $0.75, driven by seasonal strength and increasing optical component demand.

* **Calendar Q1 2025 (FY25 Q3):** Revenue growth is expected to continue, reaching $410M - $440M, with EPS in the range of $0.65 - $0.80, as AI infrastructure build-outs accelerate.

* **Calendar Q2 2025 (FY25 Q4):** Anticipated revenue of $420M - $450M, with EPS of $0.70 - $0.85, completing a year of strong recovery and growth.

* **Calendar Q3 2025 onwards (FY26 & beyond):** While specific quarterly estimates for further out periods can vary, analysts project substantial full fiscal year growth. FY26 (July 2025 - June 2026) is expected to see revenue growth in the high teens percentage range, potentially reaching $1.7B - $1.8B, with EPS growing even faster to $3.00 - $3.25+. This growth will be fueled by sustained AI demand, the rollout of 800G and 1.6T optical transceivers, and a broader recovery in enterprise and telecom spending, leading to continued sequential improvements in calendar Q4 2025, Q1 2026, and Q2 2026.

### Recent Catalysts

* **AI/Machine Learning Infrastructure Build-out:** Explosive demand for high-speed, high-density optical interconnects (e.g., 800G and beyond transceivers) to support AI data centers is creating a significant tailwind for Lumentum's optical communications segment.

* **Next-Generation Optical Networking:** Continued global deployment of 5G and fiber-to-the-home (FTTH) networks, along with upgrades to core and metro networks, drives demand for Lumentum's advanced optical components.

* **New Product Introductions:** The company's ongoing innovation and introduction of higher-speed and more efficient optical components are capturing new design wins and expanding market share.

* **Recovery in China and Enterprise:** Signs of stabilization and potential recovery in the Chinese telecom market and enterprise spending could provide additional uplift.

### Main Risks

* **Market Cyclicality:** Lumentum operates in cyclical markets, particularly telecom and data communications. Economic slowdowns or oversupply in certain segments can impact demand and pricing.

* **Intense Competition:** The optical components and laser markets are highly competitive, with established players and emerging entrants vying for market share, potentially leading to pricing pressure.

* **Supply Chain Disruptions & Geopolitical Tensions:** Reliance on a global supply chain makes the company vulnerable to disruptions, while geopolitical issues (e.g., trade restrictions, export controls) can impact sales and operations.

* **Customer Concentration:** A significant portion of revenue may come from a few large customers, making the company susceptible to their purchasing decisions and market fluctuations.

* **Technological Transitions:** Rapid technological advancements require continuous R&D investment. Failure to innovate or adapt to new industry standards could erode competitive advantage.