NBTX Breakout Report

Investor Analysis

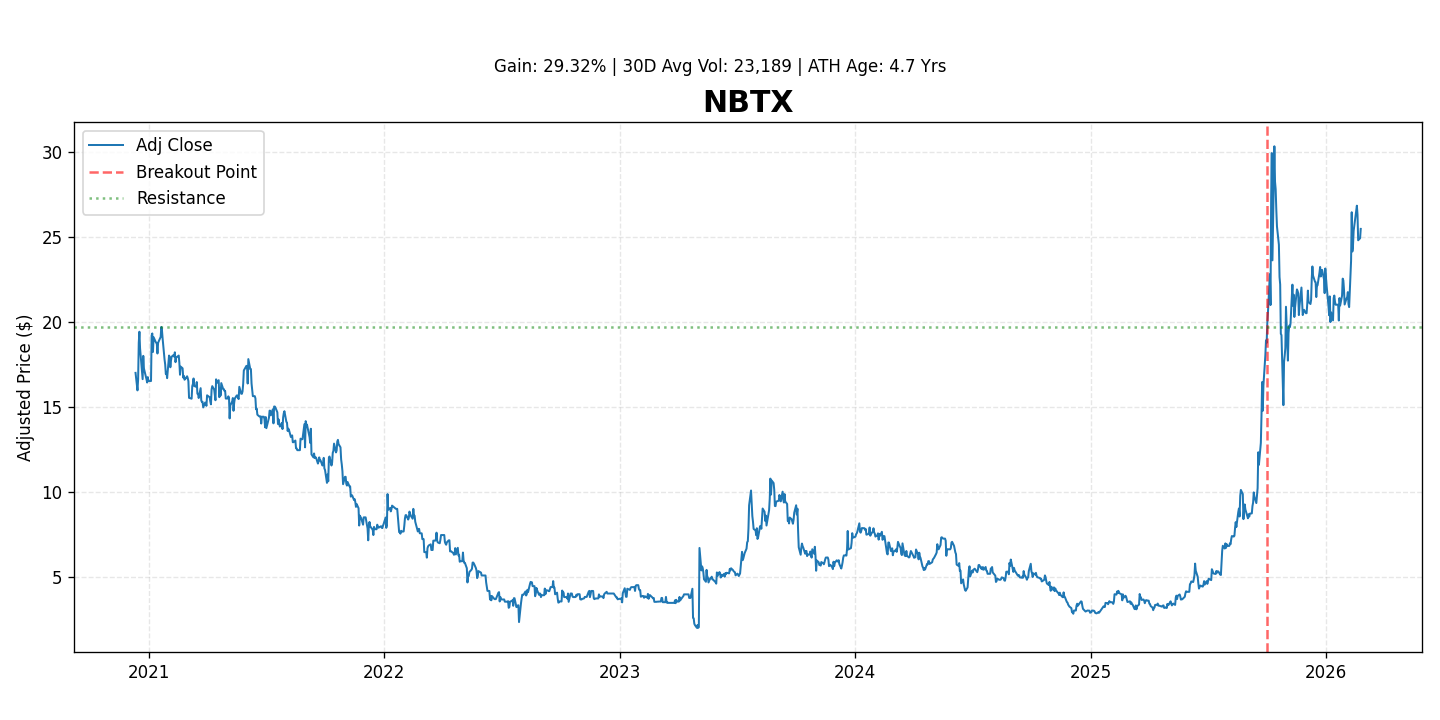

Investor Summary: Neumora Therapeutics (NBTX)

Neumora Therapeutics (NBTX) is a clinical-stage biopharmaceutical company focused on developing precision medicines for brain diseases. The company leverages an integrated data science platform to identify novel targets and patient populations, aiming to address the significant unmet needs in neuropsychiatric and neurodegenerative disorders. The stock has demonstrated strong market momentum, gaining 29.3% since its recent breakout, reflecting growing investor optimism surrounding its pipeline progress and strategic approach.

Business Overview

Neumora Therapeutics is dedicated to transforming the treatment of brain diseases by combining robust data science with deep expertise in neuroscience. Its pipeline consists of multiple programs targeting genetically defined patient populations across various indications, including Major Depressive Disorder (MDD), schizophrenia, and bipolar disorder. The company's lead programs, NMRA-140 (a VMAT2 inhibitor) and NMRA-511 (a kappa opioid receptor antagonist), are currently in mid-stage clinical development for MDD, with other assets in earlier stages targeting distinct mechanisms of action.

Key Competitive Moats

- Precision Medicine Approach: Neumora's core differentiator is its proprietary data science platform, which integrates genetic, clinical, and imaging data to identify specific biomarkers and patient segments, aiming to increase clinical trial success rates and develop highly targeted therapies.

- Diverse Pipeline: A multi-asset pipeline spanning various brain disorders and mechanisms reduces single-point failure risk and offers multiple shots on goal for commercial success.

- Experienced Leadership: The company is led by a team with extensive experience in neuroscience drug discovery, development, and commercialization from leading pharmaceutical and biotech companies.

- Strategic Partnerships: Strong backing from prominent investors and potential for future strategic collaborations enhance financial stability and provide access to broader resources.

- Intellectual Property: Developing novel compounds and leveraging biomarker-driven approaches provide intellectual property protection for its therapeutic candidates.

Revenue and Earnings Outlook (2025-2026 Quarters)

As a clinical-stage biopharmaceutical company, Neumora Therapeutics is currently pre-revenue from product sales and is expected to continue investing heavily in research and development. Therefore, traditional revenue and earnings growth are not anticipated in 2025 and 2026. Analyst consensus estimates reflect this profile:

- Q1 2025: Revenue (primarily from potential collaborations/grants): Est. $1.0 - $3.0 million. EPS: Est. -$0.65 to -$0.75.

- Q2 2025: Revenue: Est. $1.0 - $3.0 million. EPS: Est. -$0.65 to -$0.75.

- Q3 2025: Revenue: Est. $1.0 - $3.0 million. EPS: Est. -$0.65 to -$0.75.

- Q4 2025: Revenue: Est. $1.0 - $4.0 million. EPS: Est. -$0.65 to -$0.75.

- Q1 2026: Revenue: Est. $1.0 - $4.0 million. EPS: Est. -$0.70 to -$0.80.

- Q2 2026: Revenue: Est. $1.0 - $4.0 million. EPS: Est. -$0.70 to -$0.80.

- Q3 2026: Revenue: Est. $1.0 - $4.0 million. EPS: Est. -$0.70 to -$0.80.

- Q4 2026: Revenue: Est. $1.0 - $5.0 million. EPS: Est. -$0.70 to -$0.80.

Note: These figures represent analyst consensus estimates for a pre-commercial company and are highly dependent on clinical trial outcomes, potential collaboration milestones, and ongoing R&D expenses. Significant product revenue is not projected until later-stage clinical success and potential commercialization.

Recent Catalysts

- Positive Clinical Trial Readouts: Anticipated data from ongoing Phase 2b trials for NMRA-140 in MDD (expected mid-2024 to early 2025) and progression of NMRA-511 and NMRA-092 programs are key value drivers.

- Strategic Financing & Capital Strength: Successful capital raises demonstrating investor confidence and providing runway for clinical development.

- Pipeline Advancements: Initiation of new clinical studies or advancement of existing programs into later stages signals continued progress.

- Market Recognition: The stock's recent gain of 29.3% since its breakout reflects increasing market confidence and attention to its precision medicine platform and pipeline potential.

Main Risks

- Clinical Trial Failure: Drug development, especially in neuroscience, carries a high risk of failure at any stage. Any lead program failing to meet endpoints would significantly impact the company.

- Regulatory Hurdles: Obtaining regulatory approvals (e.g., FDA) is a complex and lengthy process, with no guarantee of success even with positive clinical data.

- Funding Risk & Dilution: Sustaining extensive clinical trials requires substantial capital. Future capital raises may lead to shareholder dilution if not offset by significant pipeline progress.

- Competition: The neuropsychiatric landscape is competitive, with large pharmaceutical companies and other biotechs developing treatments for similar indications.

- Commercialization Risk: Even if approved, market adoption and commercial success are not guaranteed, facing challenges in payer coverage and physician acceptance.

- Biomarker Validation: The success of the precision medicine approach relies heavily on the robustness and clinical utility of identified biomarkers, which require rigorous validation.