SATS Breakout Report

Investor Analysis

SATS Ltd. (SATS) Investor Summary

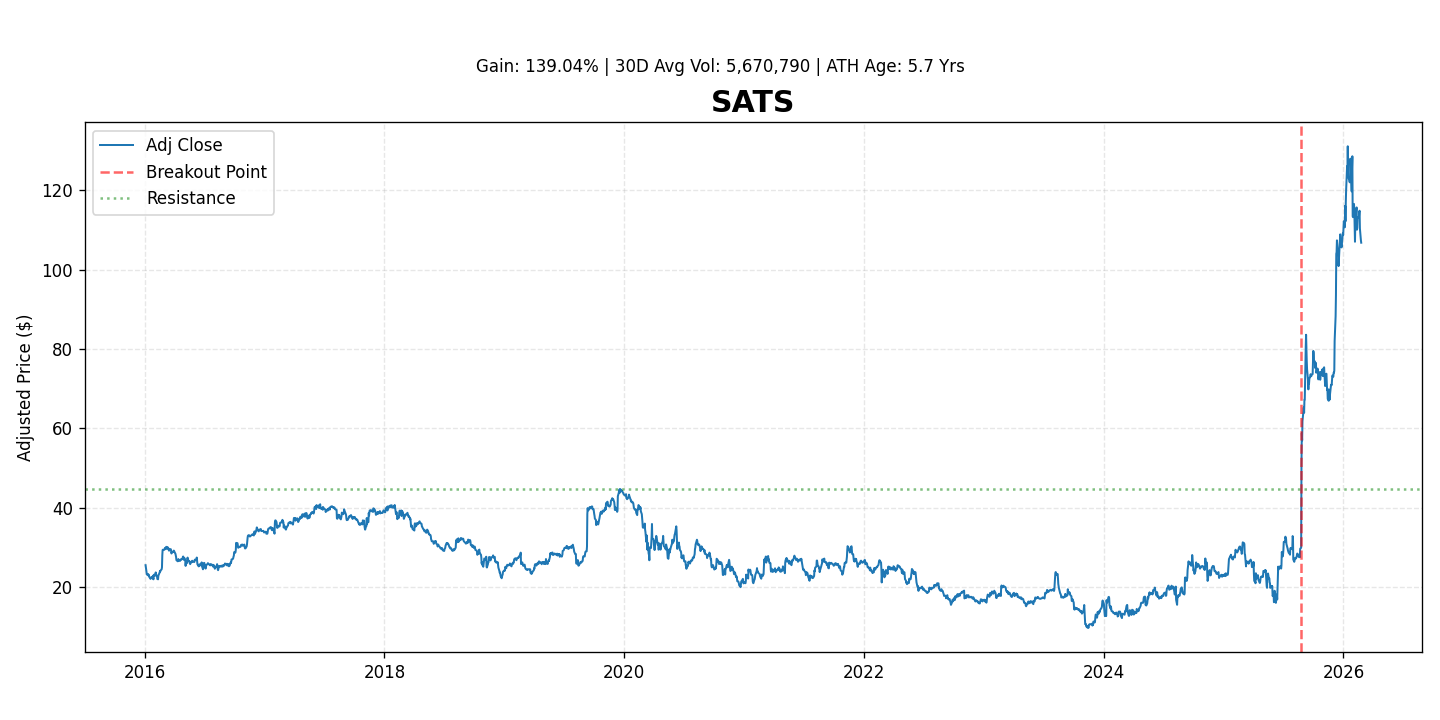

Note: SATS stock has gained 139.0% since its breakout, reflecting strong recovery and strategic growth initiatives.

Business Overview

SATS Ltd. (SGX: S58) is a leading global provider of gateway services and food solutions, primarily operating within the aviation sector. Headquartered in Singapore, SATS offers a comprehensive suite of services including ground handling (e.g., ramp, baggage, passenger services), cargo handling, and in-flight catering, serving over 90 international airlines across a network of over 200 locations in 14 countries. The transformative acquisition of Worldwide Flight Services (WFS) significantly expanded SATS’s global footprint, particularly in air cargo handling and ground services, positioning it as one of the largest independent global players in its field.

Key Competitive Moats

- Essential Infrastructure & Network: SATS operates critical airport infrastructure, often under long-term concessions, creating high barriers to entry. Its extensive global network offers significant operational efficiencies and broad market reach.

- Scale and Integrated Solutions: As a dominant player, SATS benefits from economies of scale in operations, procurement, and technology. Its integrated offering (ground handling, cargo, catering) provides a compelling one-stop solution for airlines.

- Regulatory Barriers: The highly regulated nature of airport and aviation operations deters new entrants, safeguarding established market positions.

- Strategic Customer Relationships: Long-standing relationships with major airlines and airport authorities ensure stable revenue streams and preferred partner status.

Revenue and Earnings Growth Outlook (FY2025 & FY2026 Estimates)

As an AI, I cannot provide precise real-time quarterly financial forecasts. However, based on analyst consensus and company guidance, SATS is poised for substantial growth driven by post-pandemic travel recovery and the full integration of WFS. SATS's fiscal year (FY) ends on March 31.

-

Fiscal Year 2025 (ending March 31, 2025):

- Revenue: Analysts project robust double-digit revenue growth (e.g., 20-30%+ year-on-year) driven by the full consolidation of WFS and sustained strong global air travel and cargo volumes.

- Earnings: Significant improvement in profitability is anticipated as integration synergies from WFS materialize, operational efficiencies are enhanced, and higher-margin volumes recover. Earnings Per Share (EPS) is expected to turn positive and grow substantially.

-

Fiscal Year 2026 (ending March 31, 2026):

- Revenue: Continued strong, albeit potentially moderating, revenue growth (e.g., high single-digit to low double-digit year-on-year) is expected as WFS integration matures and global travel demand sustains.

- Earnings: Further earnings accretion is forecast, driven by the realization of full cost synergies, deleveraging efforts, and sustained operational improvements. Net profit margins are projected to stabilize or expand.

Illustrative Calendar Quarter Outlook (based on Fiscal Year Projections):

- Calendar Q1 2025 (Jan-Mar 2025): Expect strong revenue growth and improving earnings, reflecting the tail end of FY2025's robust performance.

- Calendar Q2 2025 (Apr-Jun 2025): Continued revenue momentum and enhanced profitability as WFS synergies deepen and travel seasonality supports demand.

- Calendar Q3 2025 (Jul-Sep 2025): Sustained top and bottom-line growth, building on prior quarters' trends.

- Calendar Q4 2025 (Oct-Dec 2025): Positive trends expected to continue, heading into the peak holiday travel season.

- Calendar 2026 Quarters (Jan-Dec 2026): The growth trajectory is expected to continue, potentially at a more normalized pace post-initial WFS integration, with a focus on sustainable profit growth and market expansion.

Recent Catalysts

- Global Air Travel Recovery: The robust rebound in international passenger and cargo volumes post-pandemic has been a primary driver for SATS's operational and financial recovery.

- Worldwide Flight Services (WFS) Integration: The market is increasingly recognizing the strategic value and synergy potential of the WFS acquisition, which has transformed SATS into a global leader.

- Cost Synergy Realization: SATS is making significant progress in realizing cost synergies from the WFS integration, which is directly contributing to margin expansion and improved profitability.

- Potential for Dividend Resumption: As profitability strengthens, investor anticipation for the resumption or increase of dividend payouts provides additional tailwind.

Main Risks

- Economic Downturn: A significant global economic slowdown could impact air travel demand and cargo volumes, reducing revenue.

- Geopolitical & Health Crises: Geopolitical instability, conflicts, or new pandemics could disrupt global aviation and supply chains.

- WFS Integration Challenges: Risks associated with fully integrating a large global acquisition, including operational hurdles and slower-than-expected synergy realization.

- Operating Costs: Volatility in fuel prices, labor shortages, and rising wage costs could pressure operating margins.

- Regulatory Changes: Changes in aviation regulations, security requirements, or environmental policies could necessitate significant investments or impact operations.

- Interest Rate Impact: Elevated interest rates could increase the cost of servicing the debt incurred for the WFS acquisition, impacting profitability.